Sole Trader vs Limited Company: Key Differences Explained

If you’re starting a business, one of the first decisions you’ll face is whether to trade as a sole trader or set up a limited company. Both have advantages, but the right choice depends on your goals, finances, and how you want to run your business.

Which Should You Choose?

Sole trader is best if you want something simple, flexible, and low-cost.

Limited company is better if you want to grow, reduce tax, and protect personal assets.

Sole Trader

- Easy to set up – quick registration, minimal paperwork.

- You’re the business – no legal separation between you and the business.

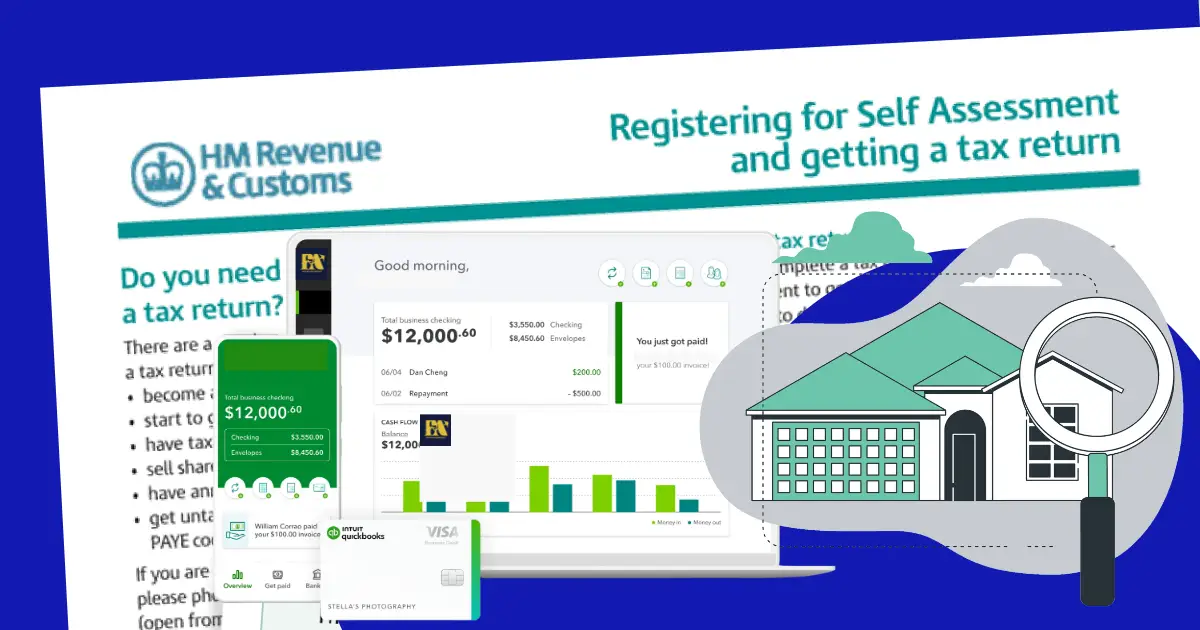

- Tax – profits are taxed as personal income through Self Assessment.

- Control – you make all the decisions, keep all profits.

- Liability – you’re personally responsible for debts and obligations.

Limited Company

- Separate legal entity – the company is its own “person” in law.

- Limited liability – your personal assets are usually protected if the business fails.

- Tax efficient – profits are taxed via Corporation Tax, and you can pay yourself through salary and dividends.

- Professional image – some clients prefer working with companies.

- More admin – must file annual accounts, confirmation statements, and follow company law.

Many people start as sole traders and later switch to a limited company as their business expands.